Compounding is the ability of an asset to generate earnings, which are then reinvested or remain invested with the goal of generating their own earnings. In other words, compounding refers to generating earnings from previous earnings. This is a very popular strategy adopted by investors to generate profits from the already generated profits which is often compounded monthly, quarterly, semiannually or annually. With continuous compounding, any interest earned immediately begins earning interest on itself. Albert Einstein allegedly called compounding interest “the greatest mathematical discovery of all time.” This is true partly because, unlike the trigonometry or calculus you studied back in high school, compounding can be applied to everyday life.

The wonder of compounding (sometimes called “compound interest”) has the potential to transform your working money into an income-generating tool. Compounding is the process of generating earnings on an asset’s reinvested earnings. To work, it requires three things: the original investment remain invested, the reinvestment of earnings and time. The more time you give your investments, the more you may be able to accelerate the income potential of your original investment.

If you invest $10,000 and it returns 6%, you will have $10,600 in one year ($10,000 x 1.06). Rather than withdraw the $600 gained, you keep it in there for another year. If you continue to earn the same rate of 6%, your investment will grow to $11,236 ($10,600 x 1.06) by the end of the second year. Because you reinvested that $600, it works together with the original investment, earning you $636, which is $36 more than the previous year. This little bit extra may seem like peanuts now, but do not forget that you did not have to lift a finger to earn that $36. More importantly, this $36 also has the capacity to earn interest. After the next year, assuming the same 6% return, your investment would be worth $11,910 ($11,236 x 1.06). This time you earned $674, which is $74 more than the first year. This increase in the amount made each year is compounding in action: investment earnings on investment earnings and so on.

With Oxon, different trading plans offer different compounding interest percentage which increases your ROI ( Return Of Investment) thereby offering more profits to ease the burden of taxes that comes with your daily trading activities.

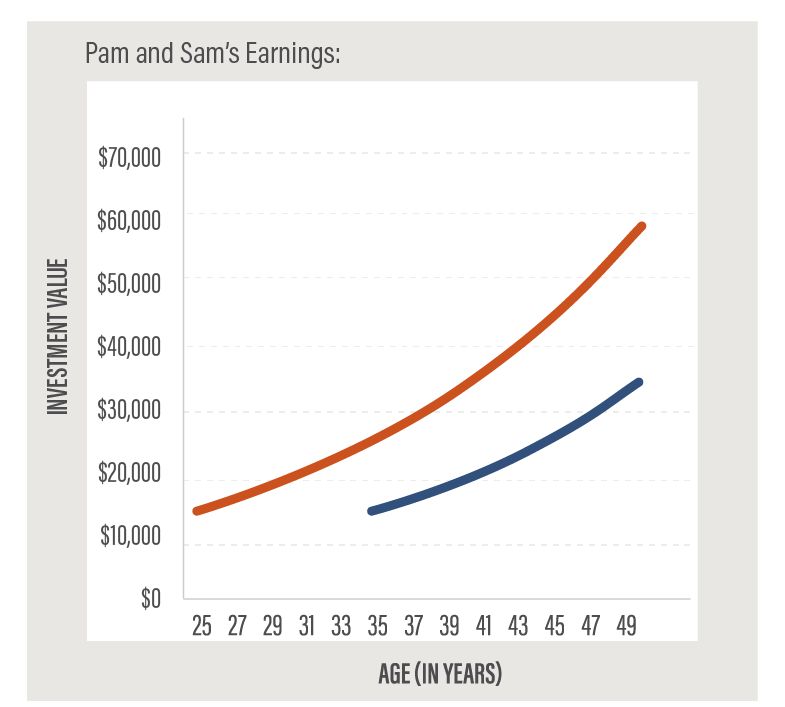

Consider two individuals; we will name them Pam and Sam. Pam and Sam are the same age.

When Pam was 25 she invested $15,000 which returned 5.5% annually. For simplicity, assume the earnings were compounded annually. By the time Pam reaches 50, her investment would grow to $57,200 ($15,000 x [1.055^25]). Pam’s friend, Sam, did not start investing until he reached age 35. At that time, he invested $15,000 which returned the same 5.5% compounded annually. By the time Sam reaches age 50, his investment would grow to $33,487 ($15,000 x [1.055^15]). What happened? Both Pam and Sam are 50 years old, but Pam’s investment earned $23,714 ($57,201 - $33,487) more than Sam’s, even though he invested the same amount of money. By giving her investment more time to grow, Pam’s investment grew by $42,201 while Sam’s investment grew by $18,487.

This hypothetical example assumes two initial $10,000 investments that earn 5.5% annually with earnings remaining invested. Pam’s investment is over 25 years and Sam’s investment is over 15 years. Taxes, management fees and other costs of investing are not reflected in this example. Results would be lower due to taxes, management fees and other costs of investing. This hypothetical example does not represent returns on any specific investment.

You can see that both investments start to grow slowly and then accelerate, as reflected in the increase in the curves’ steepness. Pam’s line becomes steeper as she nears her 50s not simply because she has accumulated more investment earnings, but because these accumulated investment earnings have been accruing additional investment earnings. In another 10 years, Pam’s line continues its steep ascent due to accrued investment earnings. At age 60, Pam’s investment would have grown to around $97,000, while Sam’s investment would have grown to around $57,000—a $40,000 difference!

The effect of compound interest depends on frequency. Assume an annual interest rate of 4%. If we start the year with $100 and compound only once, at the end of the year, the principal grows to $104 ($100 x 1.04 = $104). If we instead compound each month at 1%, we end up with more than $104 at the end of the year. Specifically, we end up with $100 x 1.0033^12 at $104.07. The final amount is slightly higher because the interest compounded more frequently.

This minor amount can really add up over the life of an investment. Compounding has the potential to positively impact the growth of your working money and maximizes the earning potential of your investments—but remember, because time and reinvesting make compounding potentially work, you should consider keeping the principal and earnings invested in order to benefit from the potential that compounding provides.